8 credit card habits that will cost you thousands

Credit cards can work for you or against you-there's no in between. They're convenient, they help you build credit, and the rewards can add up. But if you're not careful, they can quietly drain your bank account without you realizing how fast it's happening.

A lot of people think they're managing their cards responsibly, but small habits add up. Interest, fees, and missed opportunities all take a toll. These are the credit card habits that'll quietly cost you thousands if you're not paying attention.

Carrying a Balance Month to Month

One of the most expensive mistakes is carrying a balance. Even if you're making minimum payments, interest racks up fast. Most credit cards charge over 20% APR, so a $2,000 balance can snowball into hundreds in interest every year.

People often assume it's fine as long as they're "managing" it, but that ongoing balance eats into your income every single month. Paying it off in full before the due date is the best way to avoid throwing money away.

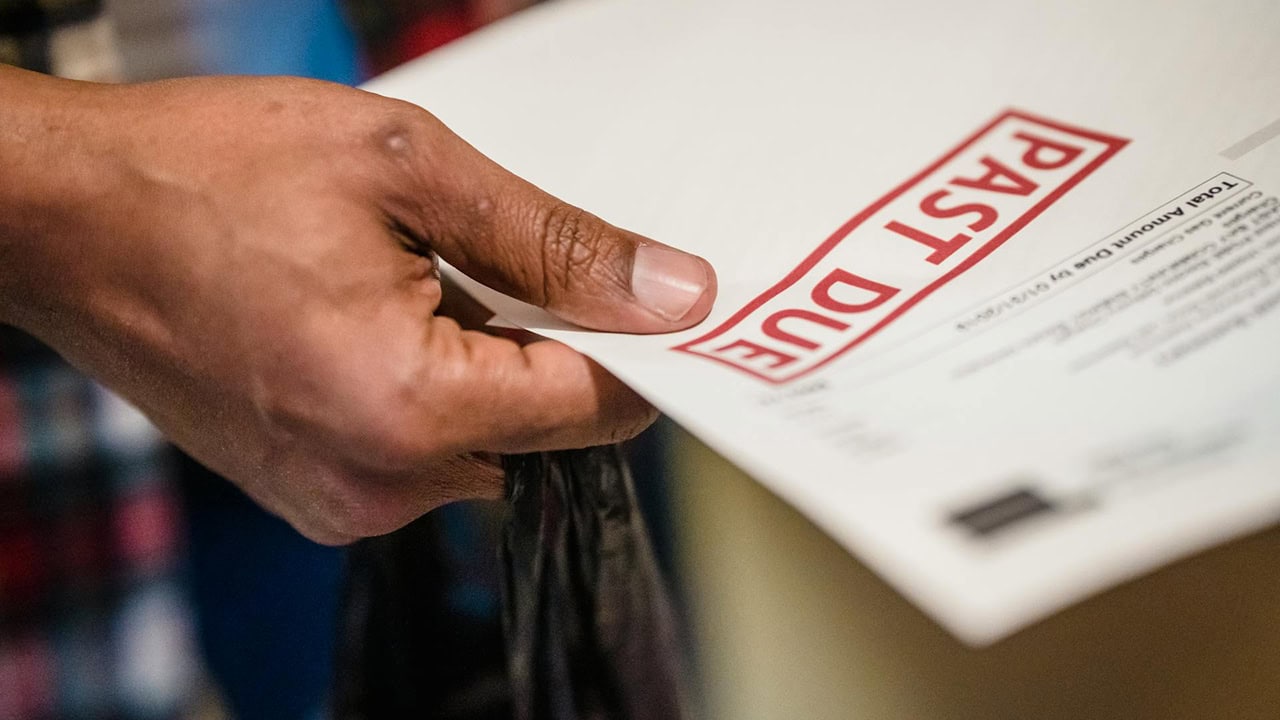

Paying Late (Even Once)

One late payment can lead to a fee, a penalty APR, and a hit to your credit score. Some cards raise your interest rate permanently after a single missed payment, which means everything you owe gets more expensive.

It also sets off a chain reaction-higher rates make it harder to pay off your balance, which increases interest, which leads to more stress. Setting up autopay or reminders can help avoid that spiral.

Ignoring the Interest Rate

If you're using a card regularly and not paying it off in full, your interest rate matters more than anything. A lot of people sign up for rewards cards or store cards without paying attention to the APR.

That's fine if you're never carrying a balance, but once you do, that 25% APR will eat into every purchase. A lower-interest card-even without perks-can save you way more in the long run.

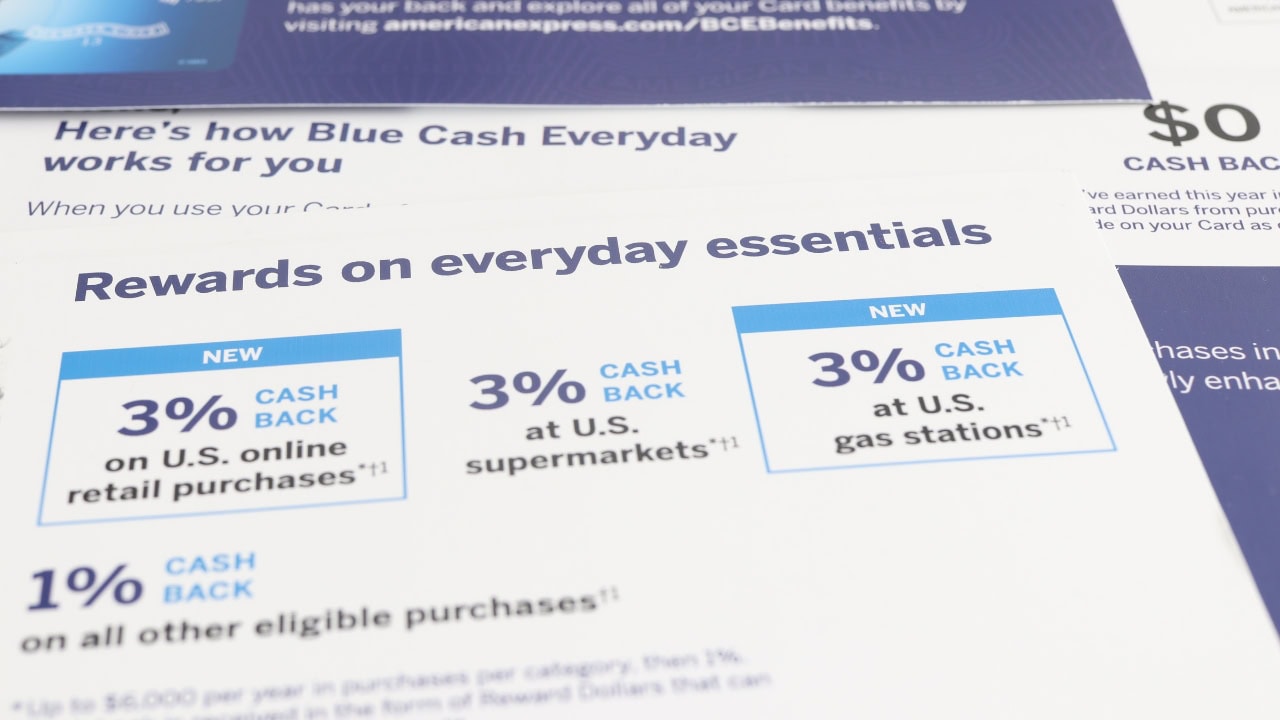

Chasing Rewards You Can't Afford

Credit card rewards sound appealing, but if you're spending more than you normally would to hit a signup bonus or rack up points, you're not really saving anything.

A $500 bonus isn't worth it if you've racked up $2,000 in debt you can't pay off right away. The interest wipes out the perks fast. If rewards are the goal, they only work when you're already spending that money anyway.

Making Only the Minimum Payment

Minimum payments keep you in good standing, but they do almost nothing to lower your balance. If you're only paying the minimum, most of your money goes toward interest instead of the actual debt.

That means you'll be paying off the same $1,000 for years-and end up paying way more than $1,000 in the process. Even adding a little extra each month helps chip away faster and cuts down on what you owe in the long run.

Using the Same Card for Everything

If you use the same card for every purchase and never check your statement, you might be missing unauthorized charges, annual fees you forgot about, or sneaky rate hikes.

Using multiple cards responsibly can help you keep utilization lower and spot red flags quicker. It also gives you flexibility if one card has a better deal or lower rate for certain types of purchases.

Taking Out Cash Advances

Cash advances are one of the worst things you can do with a credit card. There's no grace period, interest starts immediately, and the APR is often higher than your normal purchases.

On top of that, there's usually a hefty fee-often 3% to 5% of whatever you withdraw. If you're tight on cash, there are better options like a personal loan or asking your bank for overdraft protection instead.

Letting Your Utilization Get Too High

Even if you don't hit your limit, using too much of your available credit makes lenders nervous. A high credit utilization ratio-especially above 30%-can drag down your credit score fast.

That not only affects your ability to get loans later, but it can also mean higher rates on insurance, deposits, or housing. Paying down your cards or asking for a higher credit limit can help lower that ratio without adding new debt.

*This article was developed with AI-powered tools and has been carefully reviewed by our editors.

Leave a Reply