10 things that will wreck your credit score without you knowing

Your credit score affects way more than loan approvals-it can mess with your interest rates, your ability to rent a place, or even your insurance premiums. But what's frustrating is that it doesn't always tank from obvious things. Sometimes it's the little stuff, the stuff that feels harmless or gets overlooked, that does the most damage.

If you're not paying close attention, you could be hurting your score without even realizing it. These are the habits and oversights that quietly chip away at it over time.

Paying Bills Late by a Few Days

Even one late payment can ding your credit score if it hits that 30-day late mark. Some lenders report it immediately, and that stays on your credit report for years.

You might think you're safe if it's just a couple of days behind, but depending on the company, even that can come with penalties and interest that snowball. Setting up auto-pay or reminders makes a big difference here. It's not always about the amount-it's the timing that gets you.

Closing Old Credit Cards

It sounds smart to close accounts you don't use, but that can backfire fast. Your credit score is partly based on the age of your accounts and your overall credit limit.

When you close an old card, you lose that history and shrink your available credit. That can raise your credit utilization ratio, even if you haven't taken on new debt. If the card doesn't have an annual fee and you're not tempted to use it, it might be better to leave it open.

Using Too Much of Your Credit Limit

Maxing out your credit cards-or even coming close-can cause a dip in your score. Even if you're making payments on time, high utilization makes you look riskier to lenders.

Experts usually recommend keeping your usage under 30% of your total available credit, but lower is even better. A high balance relative to your limit can signal overextension, even if you plan to pay it off soon. That snapshot in time still matters.

Only Making the Minimum Payment

Paying the minimum keeps you in good standing, but it does little to chip away at your balance. It also signals that you may be stretched too thin, especially if you're carrying a high balance month to month.

Over time, interest adds up, and your utilization stays high, which can drag down your score. Even small extra payments each month can help lower that balance faster and show more positive credit behavior.

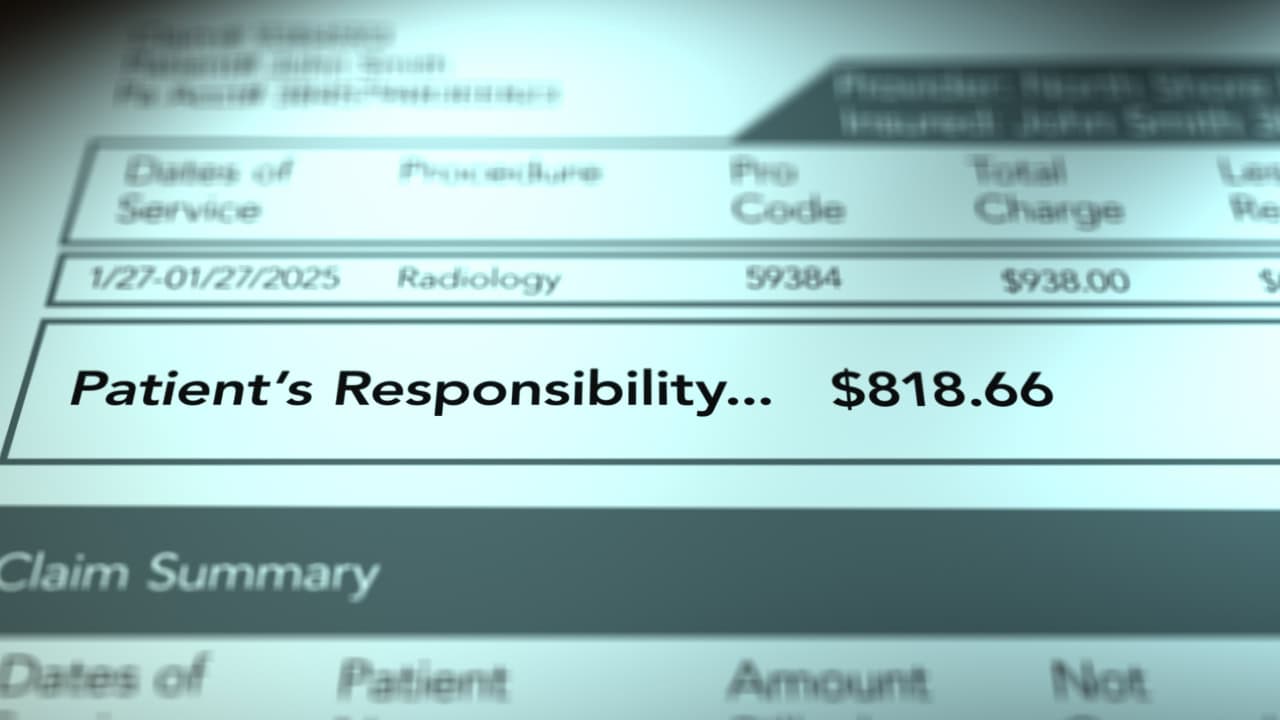

Ignoring Medical Bills

Medical bills might not feel like “real” debt at first, but if you ignore them long enough, they can end up on your credit report. Once they're sent to collections, the damage is done.

Some credit scoring models have gotten better about handling medical debt, but not all lenders use the newest versions. If you're overwhelmed by a bill, ask for a payment plan or financial assistance. Don't assume it'll disappear on its own.

Applying for Too Many New Accounts

Every time you apply for a new credit card or loan, it triggers a hard inquiry. One or two won't hurt much, but several in a short window can raise red flags.

It looks like you're desperate for credit or taking on too much at once, which makes lenders nervous. If you're shopping around for rates, try to keep your applications within a short timeframe so they get grouped together.

Co-Signing Someone Else's Loan

When you co-sign, their debt becomes your responsibility too-even if you never touch it. If they make a late payment or default, your credit takes the hit right alongside theirs.

It also shows up on your credit report as your own obligation, which affects your debt-to-income ratio. Even if everything goes well, that account can limit your ability to qualify for other credit in the meantime.

Not Checking Your Credit Reports

Mistakes happen. And if you're not checking your credit reports regularly, you might not notice a problem until it's already wrecked your score. Fraudulent accounts, incorrect balances, or outdated info all show up more than people think.

You can get free reports from all three major bureaus once a year through AnnualCreditReport.com. Set a calendar reminder and look through everything carefully. Catching something early makes it way easier to fix.

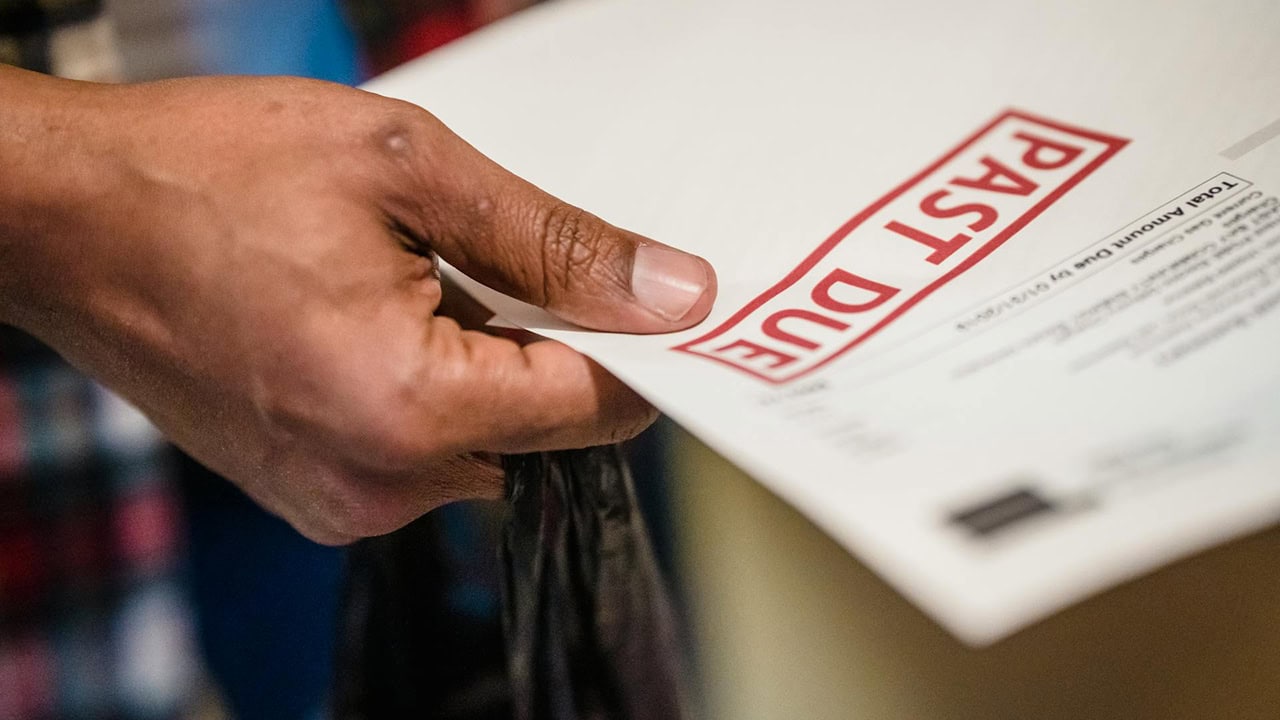

Letting a Bill Go to Collections

Even small debts, like an old utility bill or forgotten subscription, can end up in collections if they go unpaid. And once they're there, your credit takes a serious hit.

Collection accounts stay on your report for up to seven years. Even if you eventually pay them off, the damage is already done. Make sure you're not missing final bills when you move or cancel services.

Having Only One Type of Credit

Your credit mix matters more than most people realize. If all you've ever had is a credit card, lenders can't see how you handle other types of debt like installment loans.

You don't need to go open random accounts just to mix things up, but adding a car loan or student loan into the mix over time can help round out your profile. A healthy credit history shows you can handle different types of payments responsibly.

*This article was developed with AI-powered tools and has been carefully reviewed by our editors.

Leave a Reply